Introducing 9A1 Capital

This blog aims to share our refined philosophy and approach to public and stock market investing, which has been shaped by over a decade of experience in both public and private markets.

We intend to offer insights into how we manage our proprietary portfolios and assess our performance using widely recognized benchmarks. Our purpose is to challenge ourselves, firmly believing that our portfolio approach will generate superior returns over the long term while remaining mindful of the inherent risks associated with stock market investing.

Simplicity is a core value in our writing. We have come to appreciate, after more than ten years of investing, that the art of investing, like many remarkable endeavors, is fundamentally simple.

However, before delving into the specifics of our investment strategy and practices, we find it essential to outline the overarching principles that form the foundation of our approach.

We prioritize a significant margin of safety in our investment approach, which essentially means that we seek substantial room for error. We firmly believe that the foundation for making money lies in the entry phase. Therefore, we make our moves when an investment opportunity lacks popular appeal and is available at an attractive price point.

We place great emphasis on the role of the promoter or management in unlocking growth potential. Consequently, our due diligence often involves spending time with management, analyzing their track record in relation to minority shareholders, and assessing their actions such as promoter buying and remuneration structure to gauge their alignment of interests.

Once we make an investment, our intention is to hold it indefinitely, unless there is a significant change in circumstances. We firmly believe that entities or individuals experiencing growth will likely continue on that trajectory, and it is best to refrain from interrupting the process unnecessarily.

We have learned from past experiences that selling stocks based on the completion of a particular story or high valuation has often led to regret.

We are willing to hold our investments for years if our original investment thesis is unfolding as expected, even if the returns may come in irregular bursts.

Our approach also involves mitigating risks by carefully studying factors such as debt profiles, revenue concentration, and other relevant aspects.

Our goal is for the investment opportunity to be easily understandable, to the point where we could explain it to a five-year-old, indicating it as a clear and compelling opportunity aka a “Screaming Buy”

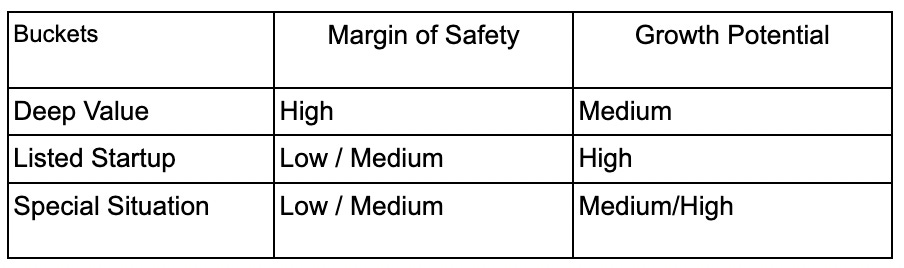

In anticipation of the post becoming lengthy, we will briefly outline three buying buckets that provide an ideal risk/return mix and share an idea from each. Future posts will delve into each bucket and our capital allocation approach

Case Study 1 - A Deep Value Buy

This company emerges from a prominent South Indian group. This company combines its core business with strategic investments, offering exposure to construction materials, cement, and technology sectors.

See if you can figure out from the following clues -

Clue 1: Market Capitalization Secrets

The company boasts a market capitalization in the single-digit thousand crores range. Its modest size holds hidden potential for clever investors to uncover.

Clue 2: Unconventional Investment Footprint

Revealing an unexpected twist, the company holds investments valued at twice its market capitalization. This distinct approach showcases a diversified investment portfolio beyond the norms of a typical holding company.

Clue 3: Revealing Revenue

Surpassing its market capitalization, the company's revenue signifies its robust market presence and growth prospects.

Clue 4: Profitability Puzzle

With consistent profitability ranging from 8-10% of its revenue, the company demonstrates sound financial performance and management.

Clue 5: Debt Dynamics

The company manages debt levels that are three times its annual profit after tax (PAT), highlighting a balanced approach to leveraging opportunities while ensuring prudent risk management.

Case Study 2: Unveiling a Listed Company with Startup-like Growth

This company operates under the umbrella of a huge financial corporation, benefitting from synergies that enhance its growth potential.

Clue 1: Market Capitalization:

With a market capitalization of fewer than 100 crores, this company possesses a modest valuation that belies its remarkable growth prospects.

Clue 2: License Advantage:

Distinguishing itself further, the company holds both Asset Management and Wealth Management licenses. This strategic advantage enables it to tap into lucrative markets and offer comprehensive financial solutions to its clients.

Clue 3: Executive Appointment:

Recently, the company made a significant move by appointing a top-level executive from one of India's largest banks. This seasoned professional brings valuable expertise and experience to spearhead the expansion of the company's business operations.

This listed company, characterized by its startup-like growth trajectory, is poised to capitalize on its synergistic relationship with a larger financial corporation. With a market capitalization below 100 crores and the strategic advantage of holding Asset Management and Wealth Management licenses, the company's recent executive appointment signals a commitment to expanding its business horizons.

Case Study 3: Unveiling a Turnaround-Based Special Situation

Operating within the iron-steel processing industry, this company manages an efficient processing facility, which forms the cornerstone of its operations.

Clue 1: Market Capitalization:

With a market capitalization below 100 crores, the company presents an undervalued investment opportunity, primed for potential growth.

Clue 2: Debt Restructuring:

Recently, the company completed a One Time Settlement (OTS) that significantly reduced its debt burden by over 70%. This achievement marks a pivotal milestone in the company's turnaround strategy. Moreover, it successfully secured refinancing through a Special Assets Fund, providing much-needed financial stability.

Clue 3: Revenue Potential:

Impressively, the company's trailing twelve-month (TTM) revenue surpasses ten times its market capitalization. This underscores the significant revenue potential and sets the stage for enhanced profitability.

Clue 4: Attractive Valuation:

The company's price-to-book value stands below 0.25, suggesting a compelling undervaluation. This favorable valuation metric further enhances the investment appeal.

Happy to chat and discuss these in detail

About Us -

Govind Shorewala - Entrepreneur (Mining, Textiles) & Investor (Private & Public Markets) → Reachout at: govind.shorewala@gmail.com

Aaroah Mittal - Early Stage VC → Reach out at: aaroah.m@people-group.com